Key takeaways

- Choosing to start your public pensions and retiring from work are two different things.

You can delay both the Old Age Security (OAS) and Canada Pension Plan (CPP) and start them at different ages.

- You can start your CPP retirement pension and continue contributing to the plan up to age 70 and earn Post-Retirement Benefits (PRBs).

- If you want or need your retirement pension earlier, the PRB could be an excellent way to increase your retirement income.

Each PRB gives a small boost that's payable for life and fully protected against inflation.

- Like the retirement pension, PRB amounts increase based on the age you start taking them.

This means that PRBs earned later in life are worth more.

- You can get more lifetime CPP income by taking CPP retirement pension at age 65 and contributing to PRBs until age 70.

If you delay your CPP retirement pension until age 70, you will get the largest monthly amount.

Overview

Keith worked in construction all his life and just accepted a new site job at 60. Keith has some savings, but still plans to work until at least age 70. Keith wants to know what the best strategy for his Canada Pension Plan (CPP) retirement pension and Old Age Security (OAS) pension will be.

How did Keith find his monthly CPP and OAS amounts?

Keith went to My Service Canada Account to see his personal statement of contributions. He saw what his estimated CPP retirement pension at age 65 would be.

For his expected OAS pension he went to OAS benefits estimator.

What is the PRB?

If you work while collecting your Canada Pension Plan (CPP) retirement pension, you can also collect CPP Post-Retirement Benefits (PRBs). Each year that you work and contribute, you will collect a small top-up from an additional PRB that will be added to your CPP retirement pension and benefits. Each PRB is adjusted based on your age when you start receiving it. If you are younger than 65, that PRB will be reduced. If you're older than 65, a new PRB is worth more.

To learn more how we top-up your CPP retirement pension using PRBs, visit our Main sources of retirement income page.

What are Keith's choices to combine his CPP retirement pension with PRBs?

Choice 1: Take Canada Pension Plan (CPP) retirement pension at age 60 for the lowest monthly pension. Keith will continue working and contributing until age 70 and collect 10 Post-Retirement Benefits (PRBs).

Choice 2: Take CPP retirement pension at age 60 for the lowest monthly pension. Keith will continue working until age 70 but stops contributing at age 65 and collect just 5 PRBs.

Choice 3: Take CPP retirement pension at age 65 and continue contributing to the CPP until age 70. This will give Keith 5 PRBs.

Choice 4: Take CPP retirement at age 70 for the highest monthly pension, without PRBs.

What are the monthly CPP retirement pensions for each choice?

Choice 1: Take CPP at 60, contribute to 70.

Choice 2: Take CPP at 60, contribute to 65.

Choice 3: Take CPP at 65, contribute to 70.

Choice 4: Contribute to 70, take CPP at 70.

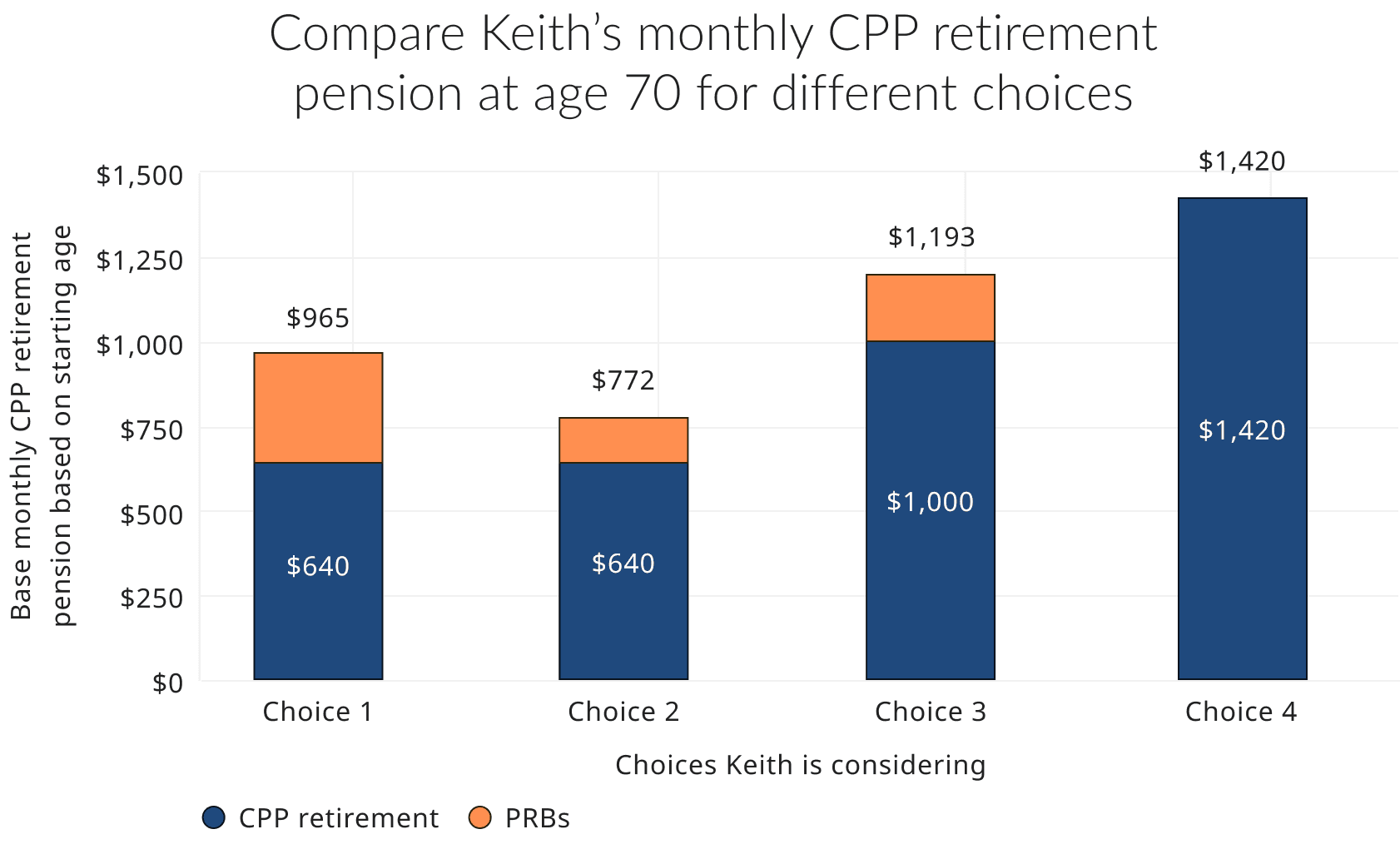

Text alternative for Compare Keith's monthly CPP retirement pension at age 70 for different choices

Description

This chart shows four choices Keith has for his monthly retirement income. He has two potential sources of income between his CPP retirement pension and his Post-Retirement Benefits. For all choices, the CPP retirement pension makes up the most of his monthly income. Taking his CPP at age 70 is the largest amount of monthly income. Taking his CPP at age 60 and continuing to work for 5 years to receive 5 Post-Retirement Benefits is the smallest amount of monthly income.

Values

| Choices Keith is considering | Base CPP retirement pension based on starting age | Amount for added PRBs | Total monthly amount |

|---|---|---|---|

| Choice 1: Take CPP at 60, contribute to 70. | $640 | $325 | $965 |

| Choice 2: Take CPP at 60, contribute to 65. | $640 | $132 | $772 |

| Choice 3: Take CPP at 65, contribute to 70. | $1,000 | $193 | $1,193 |

| Choice 4: Contribute to 70, take CPP at 70. | $1,420 | - | $1,420 |

The monthly Canada Pension Plan (CPP) retirement pension will be paid at the time when Keith applies to collect it. However, the PRBs will accumulate slowly during the years when Keith continues to work and contribute. Each year of additional contributions to the plan will result in an additional small top-up to the existing pension and benefits next year. The graph compares the pension at age 70 for different choices, and the amounts are quite different.

Choices 3 and 4 are about Keith taking his CPP retirement pension later in life, at age 65 and 70, and receiving higher monthly pension amounts. Keith would like to choose his strategy between these two options. For both options, Keith knows he will continue paying contributions until age 70.

What else should Keith consider when choosing?

When Keith is deciding when to start his public pensions, it is important he thinks about:

- his monthly amount

- the total amount he will collect over his lifetime

Before making his final decision, Keith wants to check one more thing. He wants to see how his lifetime pension will change if he starts at different ages.

What will be Keith's pension by age 87?

As Keith is still healthy and working, he should plan on living for another 22 to 25 years (age 87 to 90) or longer. He would like to choose between Choices 3 and 4.

- Choice 3 was about Keith taking his Canada Pension Plan (CPP) retirement pension at age 65 and contributing to the plan until age 70. He will have his pension monthly income earlier in life and a higher lifetime pension.

- Choice 4 was about Keith delaying his CPP retirement pension until age 70. It is also a good option since it gives the highest monthly pension and a high lifetime pension as well.

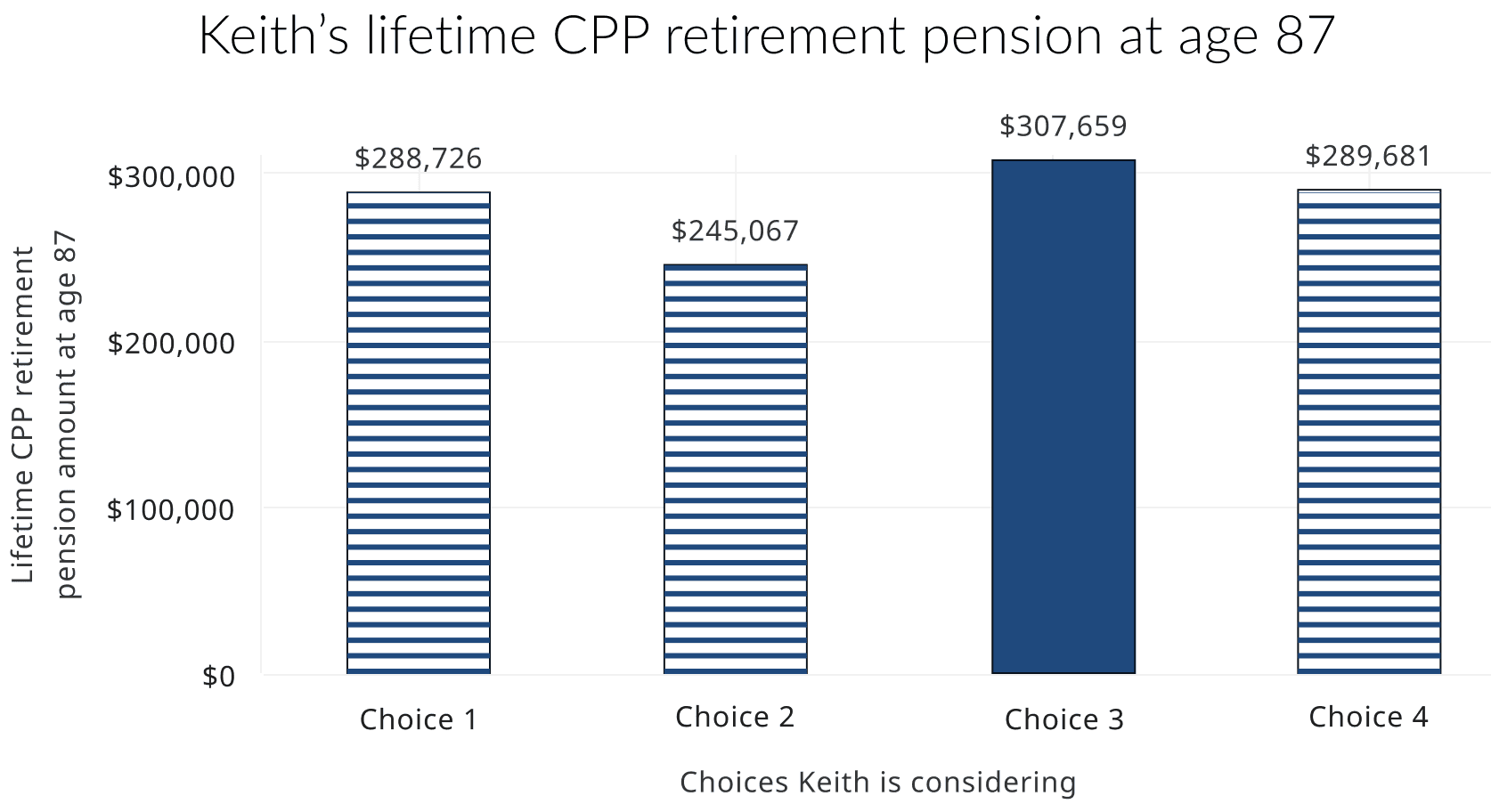

Choice 1: Take CPP at 60, contribute to 70.

Choice 2: Take CPP at 60, contribute to 65.

Choice 3: Take CPP at 65, contribute to 70.

Choice 4: Contribute to 70, take CPP at 70.

Text alternative for Keith's lifetime CPP retirement pension at age 87

Description

This chart shows the lifetime CPP retirement pension amount for 4 choices Keith is thinking about. It shows that by age 87, the choice of starting his CPP retirement pension at age 65 while working and contributing until 70 would give Keith the most retirement income.

Values

| Choices Keith is considering | Lifetime CPP retirement pension amount at age 87 |

|---|---|

| Choice 1: Take CPP at 60, contribute to 70. | $288,726 |

| Choice 2: Take CPP at 60, contribute to 65. | $245,076 |

| Choice 3: Take CPP at 65, contribute to 70. | $307,659 |

| Choice 4: Contribute to 70, take CPP at 70. | $289,681 |

Keith notices that the most commonly used Choice 2 has the lowest monthly and lifetime pensions.

What will be Keith's pension by age 90?

Keith could live a longer life and that would change his lifetime pension.

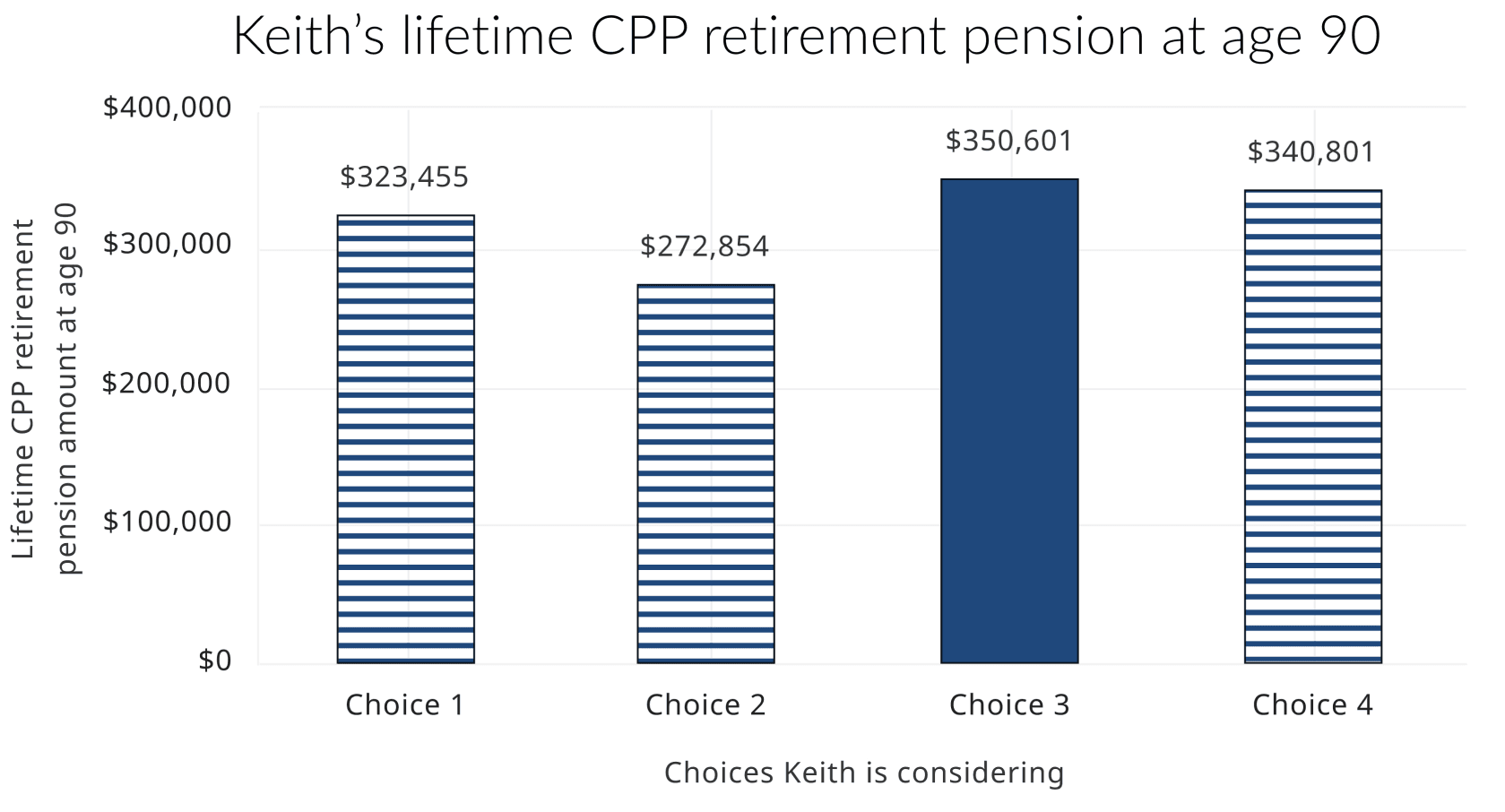

Choice 1: Take CPP at 60, contribute to 70.

Choice 2: Take CPP at 60, contribute to 65.

Choice 3: Take CPP at 65, contribute to 70.

Choice 4: Contribute to 70, take CPP at 70.

Text alternative for Keith's lifetime CPP retirement pension at age 90

Description

This chart shows the lifetime CPP retirement pension amount for 4 choices Keith is thinking about. It shows that if Keith lives to age 90, starting his CPP retirement pension at age 65 while working and contributing until 70 would give him the most retirement income.

Values

| Choices Keith is considering | Lifetime CPP pension amount at age 90 |

|---|---|

| Choice 1: Take CPP at 60, contribute to 70. | $323,455 |

| Choice 2: Take CPP at 60, contribute to 65. | $272,854 |

| Choice 3: Take CPP at 65, contribute to 70. | $350,601 |

| Choice 4: Contribute to 70, take CPP at 70. | $340,801 |

Even at age 90, Choice 3 still has the highest lifetime pension. Keith decides that taking his CPP retirement pension at age 65 and contributing until 70 is his best option.

Keith's OAS pension

Keith's income would not qualify him for the Guaranteed Income Supplement (GIS), as he will continue to work up until age 70 with good salary. The GIS is for people with low income.

Keith chooses to delay the Old Age Security (OAS) pension until age 70 to permanently increase it by 36%. This higher pension will help him transition better into retirement when he stops working at age 70.

To learn more about what to consider when choosing the age you want to start your OAS pension, read Fred decides when to start his public pensions.

Conclusion

Keith is working later in retirement and plans to stay on the job until age 70. He might not need the Canada Pension Plan (CPP) retirement pension income immediately and does not qualify for the Guaranteed Income Supplement (GIS). He wants to take the largest pensions from the Old Age Security (OAS) and CPP retirement pensions available to him. He would like to know how he can use Post-Retirement Benefits (PRBs), if he chooses to take CPP before he retires from his job.

Keith decided to start CPP at age 65 and continue contributing to age 70, receiving 5 PRBs. This choice will give a high monthly pension that will be topped up annually with up to 5 additional PRBs. And it will provide the largest lifetime pension by age 87 and 90.

Keith also decides to delay his OAS pension until age 70. The higher monthly benefit will help when he retires from work.

Learn more

Going from work to retirement

You can choose different ways to go from work to retirement. Retiring from work and starting your public pensions are two different things.

Rules of thumb for your public pensions

Check out these tips to help you decide when to start your public pensions. Choose what is right for you.

Canada Pension Plan Post-Retirement Benefit (PRB): Overview

Check here for details about the CPP Post-Retirement Benefit, who is eligible for it, how much you could receive, and how to apply.